Origination Charges | Lowest Rate is Not Always the Best Option

Most people think that getting the lowest rate possible is the best route when it comes to a mortgage. What they do not sometimes realize is that a rate is tied to origination charges such as, but not limited to:

- Underwriting Fee.

- Origination Fee.

- Mortgage Broker Fee.

- Loan Discount Points.

- Processing Fee.

- Application Fee.

One important question to answer when choosing the rate should be: How long do I think I am I going to keep this loan – taking into consideration refinancing, paying off the mortgage, or selling the home?

A lender may advertise a rate that seems appealing and some people focus on getting the lowest rate possible, but it is not always in their best interest.

Advertising Rates

When advertising rates, lenders will often put the lowest rate possible they can get away with while staying compliant. This in most cases is not realistic for a borrower because they will not have the loan long enough for this to be beneficial. A Loan Originator can calculate a break even when it comes to closing costs.

Some loan programs even have net tangible benefits to protect borrowers. For example, take into consideration a VA IRRRL – there are guidelines that in some cases need to be met in order to be complaint. The equation for determining recoupment period for a VA IRRRL is:

- (Fees + Expenses + Closing Costs) – the Lender Credit should be ≤ 36 months Reduction of Monthly Principal and Interest Payment

Recoupment should also be considered when refinancing even on other loan programs, such as:

- Conventional loan.

- Commercial loan.

- FHA loan.

- Hard money loan.

- Non-qualified mortgage loan.

- USDA loan.

In most cases, depending on the cost or credit, the higher cost loan with the lower rate will have a longer recoupment period.

Lower Rate is Not Always the Better Option

Rates either credit a borrower, cost money, or offer a par baseline cost. An important question to a lender when asking for a rate should be: What is your par rate with no origination charges? A rate that is higher than other rates, in most cases, but not all will provide a larger credit for closing costs.

Each rate moves independently and sometimes there can be a rate that is lower that is crediting more than a higher rate – some would call that a discounted rate.

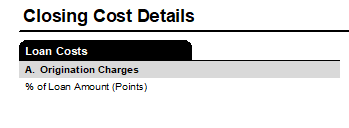

Where to Find Origination Charges Associated with the Rate

The section that outlines origination charges associated with the rate is on page 2 of the Loan Estimate in the top left corner.

The origination charges associated with rates when comparing interest rates should be taken into consideration with the following equation:

- Line A. origination charges – lender credits = net origination charges.

Recoupment Calculation Example

There are other fees associated with the loan, such as third party fees. Some of the most common, but not limited to are:

- Appraisal fee.

- Credit report fee.

- Inspection Fees.

- Title fees.

- Transfer taxes.

- Recording fee and other tax fees.

If the fees, expenses, and closing costs minus the lender credit equaled $3,982 and the savings were $198.89 per month. The total costs minus the lender credit should be divided by the savings per month – the recoupment would be 20.2 months for this example.

Choosing a rate with an appropriate recoupment period will save money.

Other Reasons Why Someone Would Refinance

In some cases, there are other reasons why people refinance such as, but not limited to:

- Cash out.

- Buyout divorce settlement.

- Home improvement.

- Removing someone from a loan.