How Do You Know if a Condo is FHA Approved | FHA Condo Mortgages

How do you know if a condo is FHA approved? Searching for an FHA loan for a condo has more moving parts than stick built homes. FHA condo approval guidelines are not difficult with the HUD’s search tool and a Loan Originators help.

If you are thinking about buying or selling, there are advantages for both when a condo is FHA approved. For a seller, it means more buyers being able to qualify which leads to more offers. For a buyer, it means an easier loan to qualify for and low down payment options.

3.5% Down Payment for a Condo

The down payment for an FHA loan for a condo is the same as a regular FHA loan.

- 3.5% for 580 or higher FICO credit score.

- 10% for lower than 580 FICO credit score.

There are even FHA grants available, with a minimum 640 FICO credit score. Not only are there advantages with FHA loans, but there are also advantages in owning a condo.

Homeownership With Convenience

Owning a home does not have to be so much work maintaining and there are benefits to owning a condo:

- Maintenance: The homeowners association usually takes over with exterior maintenance, snow removal, and shared area maintenance.

- Condos can cost less.

- Property tax insurance is usually lower than a house.

- Amenities: Depending on the complex, there can be fitness centers, security features, rooftop decks, or even pools and hot tubs.

- Location: Owning home is difficult to obtain in major cities, but condominium complexes make this more affordable and common.

- Condos tend to have cheaper insurance.

Though insurance and taxes can be cheaper, there are association dues and they all depend on what the complex has to offer.

Homeowners Association Dues

The difference between most traditional homes and an FHA condominium is that the mortgage payment will have homeowners association dues (HOA). This is a factor when determining a maximum mortgage payment even though it is usually paid outside the mortgage and not escrowed. The fee per month will depend on what the association has to offer and the condo budget.

Approval Guidelines

In order for a FHA condominium project to be FHA approved, the project must be in full compliance with applicable state laws, all other applicable laws, and regulations. Some ineligible projects include:

- Condotels.

- Timeshares.

- Non-warrantable condos.

- Multi-dwelling unit condos.

- Houseboats.

- Projects that are not residential.

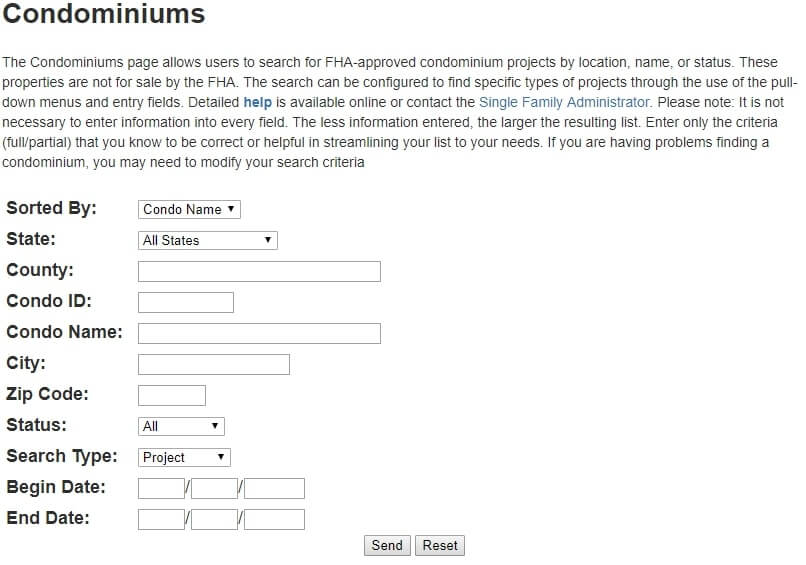

HUD’s search site makes it easy when asking the question, “How do you know if a condo project is FHA approved?” They make the process of looking for an FHA approved condo easy and not having to look through FHA guidelines.

How Do You Know if a Condo is FHA Approved

The condo search page allows anyone to look up condo projects by location, name, or status. Often, realtors or Loan Originators forget to check the status of the condo project. It is important to make sure each condo project is not only approved, but up to date. This will prevent any delays or disappointments during the underwriting process.

Starting the Loan Process

Some lenders have tougher guidelines than others. Getting pre-approved for a FHA loan for a condo starts with sending necessary documents required for underwriting and processing to a licensed Loan Originator. Once enough information has been collected, they will run the Automated Underwriting System (AUS) to determine a pre-approval purchase price and maximum mortgage payment.

{kind=link}