3 FHA Down Payment and Closing Cost Grants | FHA Grants

The FHA down payment grant is a competitively priced loan program that does not require a minimum down payment. You will gain a further understanding on:

- The FHA grant for first time home buyers.

- Grants that do not require you to be a first time home buyer.

- Advantages and disadvantages of using an FHA down payment grant.

- Closing cost grants.

Down Payment and Closing Cost Grants

They were designed for borrowers that are financially stable and have met responsibilities such as:

- Stability of employment and income.

- Managing their finances and savings.

- Exhibited responsible payments.

- Have satisfactory credit history with a minimum FICO credit score of 620.

The down payment and closing cost grants are intended for families or individuals who do not have resources available for down payment and closing costs.

The home grant programs typically have higher qualifying standards when it comes to credit and capacity than regular FHA loans.

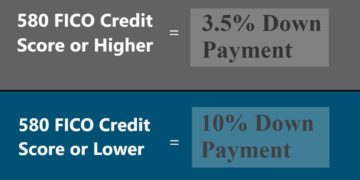

Credit Score without an FHA Grant

FHA loans will go lower on credit score:

- For borrowers with a 580 FICO credit score or higher, the minimum down payment is 3.5%.

- Borrower with under a 580 FICO credit score, the minimum down payment is 10%.

3% to 6% Down Payment and Closing Cost Grant

The 3% and 6% down payment assistance program can be applied to the down payment and/or closing costs. The grant is in form of a second lien and forgiven at month 61 with no repayment required. There is no form of repayment during the 61 months if you remain current on your mortgage.

The down payment FHA grant funds are available for 3% to 6% of the total loan amount. You are not required to be a first time home buyer.

3% and 6% FHA Grant Guidelines Summary

- Minimum credit score of 640.

- 30 year fixed term.

- 1 to 4-unit residential properties allowed.

- Cannot own another 1 to 4 family residential property at the time of closing.

- Income limit is 160% of Area Median Income (AMI).

Housing history is required:

- If a borrower does not have 12 months housing history, the borrower will need 3 in reserves.

- This is not required on the conventional home grant program.

Another Option – 2% and 3.5% Grant

Often, looking and comparing loan programs is the best way to find out what type of loan program is right for you. The 2% and 3.5% grant is available for the FHA new construction loan and FHA renovation programs. The minimum credit score is 620 FICO with no repayment required.

Advantages and Disadvantages

When determining if a down payment and closing cost grant is right for you, your Loan Originator can go over a break down of the advantages and disadvantages for your case scenario.

Advantages:

- The FHA grant can help pay for closing costs and the down payment.

- Allows financing for borrowers unable to save enough for the down payment and closing costs.

Disadvantages:

- Tougher on guidelines.

- Not as competitive terms as a regular FHA loan.

Getting Pre-approved for Down Payment and Closing Cost Grants

The pre-approval process starts by gathering documentation required for underwriting and processing. A Loan Originator can put together a list that fits your case scenario.

Once a Loan Originator has enough information, they will run the Automated Underwriting System (AUS) to determine eligibility findings. Once they have enough information regarding your pre-approval, they will go over a comfortable mortgage payment and financing options.

The last step is issuing a pre-approval and connecting with a realtor to start shopping for a home.

{kind=link}