FHA 203k Process Work Flow | Steps to a Successful FHA 203k Loan

Are you looking for a lender that does an FHA 203k loan? There are important details that the real estate agent and Loan Originator need to be aware of before executing a sales contract. Understanding the FHA 203k process work flow and the steps to a successful 203k loan will help speed up the loan process.

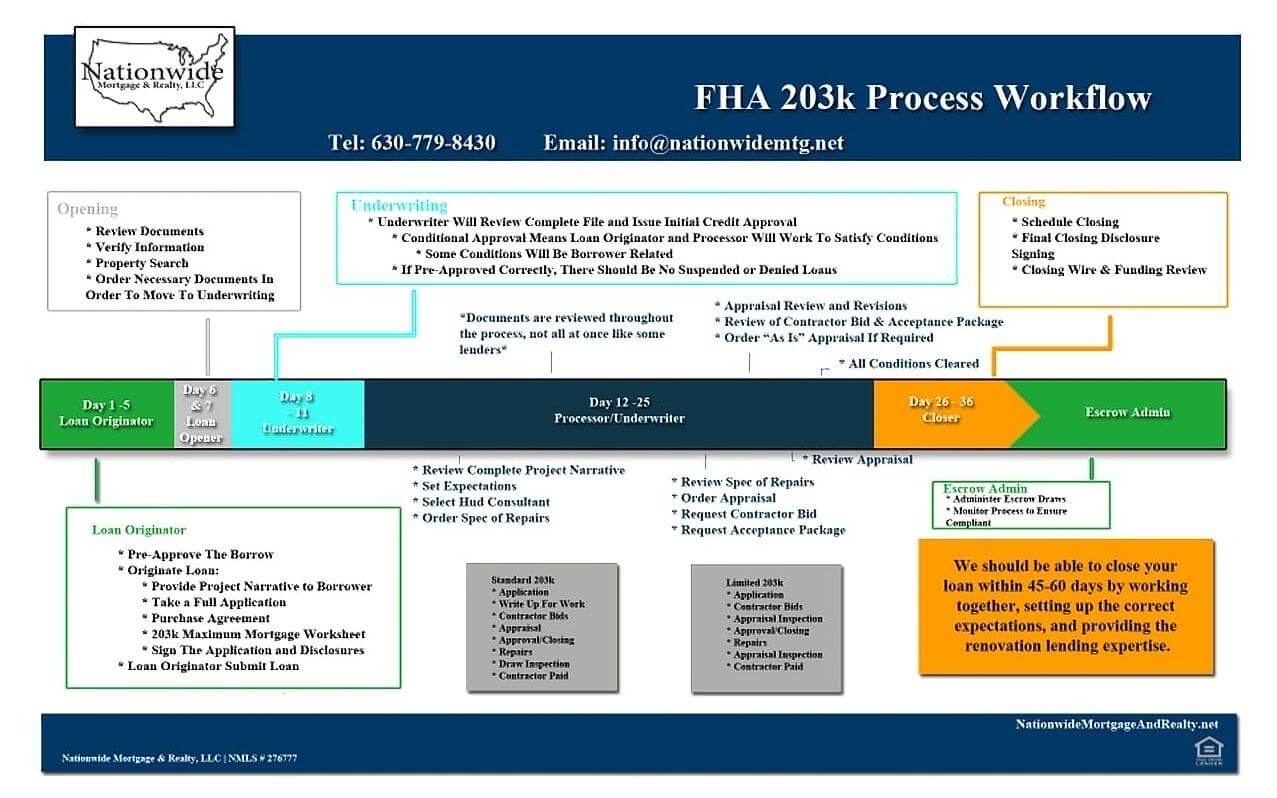

By working together, setting realistic expectations, and providing lending expertise throughout the process, an FHA 203k loan should close in 45-60 days.

Loan Origination Steps to a Successful 203k Loan

The FHA 203k process should start with a Loan Originator working through the pre-approval process with you. A solid pre-approval means that the Loan Originator took the time to go through the pre-approval steps by asking for the correct documents, reviewing the documents, and running the numbers.

Every scenario is unique when pre-approving a borrower and a pre-approval should be able to be issued the same day all documents are received.

All of the following steps should be taken:

- All requested supporting documents should be reviewed.

- Once authorization by the borrower is given, a credit report should be pulled and reviewed.

- Guidelines should be sure that they are met based on credit, debt, income, and assets.

Communication to what is going to be needed throughout the process will help speed up the FHA 203k process work flow. Running the Automated Underwriting System (AUS) to determine the findings will help limit unexpected circumstances.

Pre-approvals should not be written based on verbal information from a borrower, which often can result in a last minute denial and cancellation of a purchase agreement. The pre-approval process should be followed up with the singing of the application and disclosures once a purchase contract is executed.

FHA 203k Work Plan Narrative

The 203k work plan is a part of the FHA 203k process work flow, which is a template to help organize and communicate with a borrower to understand what the borrower would like to include in the FHA 203k loan.

- This often includes projections to help understand the needs of wanting to build additions to expand the current footprint of the home, building on the footprint, if there is any peeling paint, and if the utilities are off or winterized.

- This narrative will also spell out some common FHA required repairs, not limited to, but may include peeling paint, water damage, pest control, mold remediation, asbestos remediation, trip hazards, hand rails, and damaged drywall.

The narrative should also include any necessary repairs or desired improvements in the following:

- Interior areas: living room, family room, kitchen, appliances, dining room, master bedroom, master bathroom, other bedrooms, other bathrooms, hallway, basement, attic, and garage.

- Exterior items: driveway, roof/gutters, siding, and windows.

- Mechanical Systems: heating, air conditions, well/septic, water softener, pluming, and electrical.

Submitting a FHA 203k Loan

Once all necessary documents have been submitted, all documents will be reviewed and the FHA 203k loan will moved to underwriting. A complete file will be reviewed by an underwriter and an initial credit approval will be issued.

Once the approval is sent out, a Loan Originator and processor will have documents to follow up on and will request conditions.

- Conditions are documents that are requested by the underwriter in order to issue a clear to close.

During the underwriting process:

- The project narrative will be reviewed to set expectations, select a HUD consultant, and order the spec of repairs.

- Documents are reviewed throughout the process and not all at once like some lenders.

This will speed up the process and improve the flow of the FHA 203k Loan.

- The review spec of repairs, ordering of the appraisal, requesting the contractor bid, and the acceptance package will all be done during the underwriting process.

- Once the appraisal is complete, the appraisal will be reviewed and revisions will be requested if necessary.

Once all conditions are in and have been cleared, the FHA 203k loan will move on to the closer to schedule closing, send out a final closing disclosure, set up closing wire, and review for funding of the FHA 203k loan.

Final Steps To The FHA 203k Process Work Flow

The Escrow Administration will:

- Post closing – set up a single contact for the homeowner.

- Administer contractor draws.

- Ensure compliance with agency guidelines.

- Monitor progress.

The Difference Between a Standard and Limited 203k

The two types of FHA 203k loans are the standard FHA 203k and limited FHA 203k.

Standard FHA 203k

- Rehab costs capped at the FHA county limit.

- Maximum of one general contractor.

- Additions, alterations, and structural repairs acceptable.

- Maximum of 5 draws to the general contractor.

Limited FHA 203k

- Rehab cost capped at $35,000.

- No HUD consultant required.

- No structural work allowed.

- Maximum of up to 3 separate contractors.

- Maximum of 2 payments per contractor.

{kind=link}